The Lever Works Both Ways: Manage The Balance Sheet... And The Income Statement

Our next financial concept? OPM (other people's money).

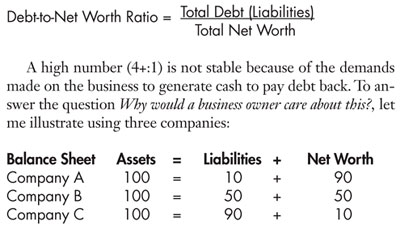

As a former commercial banker, I've had the opportunity to see both sides of the "debt/leverage" issue. When you go to a bank for a business loan, your banker (whether they tell you or not) will quickly compute your debt-to-equity ratio. As bankers, we viewed debt as an equivalent of risk: the higher your ratio, the more debt you have in proportion to equity. Therefore, the higher your financial risk. Let me explain why this is so. It all goes back to the financial basics: Assets = Liabilities + Net Worth.

An asset is something you own, and you own assets to generate sales. But to own an asset, you must buy it, and someone must provide the money. Money is provided either by creditors or owners. Bankers view the relationship between your claims and the creditors' claims against your assets with the following ratio:

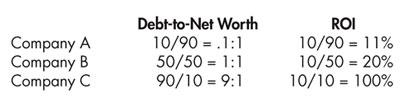

Our three companies are all the same size--that is, 100 in assets (add as many zeroes as you like). However, each firm is rather different in terms of the sources of funds to acquire its assets. Moving from Company A to Company C, it's apparent that the assets have been acquired with increasing amounts of debt, or leverage. Let's assume that each firm earns a net profit after taxes of 10. Then their return on assets (ROA) would be 10 percent. You'll notice in the following table that even though the ROA for each is 10, the return on the investment (ROI) is vastly different.

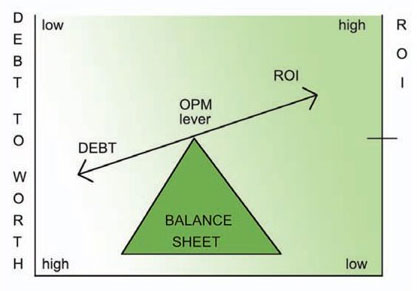

In our capitalistic society, "return" is a function of risk. Only a fool would take a bigger "risk" for a smaller return. The high return in Company C comes at the expense of a higher risk, and we see that in the form of a 9:1 debt-to-net worth ratio, or a higher leverage. The next diagram illustrates the concept of leverage.

This generally works as long as you are more profitable for having borrowed the money than if you had done nothing; this means you borrow to buy assets that will be sold to create more profits than you would otherwise have. This is called growing efficiently. Increasing debt can increase fixed and variable costs, so watch out when the pendulum swings the other way and sales fall! In that case, the lever will break in half. Then look where it will point!

My question for you is: Which company do you want to own, the company behind Door A, B, or C? How you structure your firm says a lot about you as a person. If you choose Company A, I know you like to sleep well. If you choose Company C, I know you must like to eat well--because you can't sleep! My point is that regardless of whether you're an "eater" or a "sleeper," where your firm winds up is controllable.

Working in the bank, it seemed like many of my borrowing customers focused the bulk of their efforts on "sales" and the "income statement," leaving the balance sheet to "fend for itself." Not many business owners manage the balance sheet as aggressively or effectively as they do the income statement. That is, until the balance sheet sucks cash out of the profit-and-loss statement faster than the P&L can produce it.

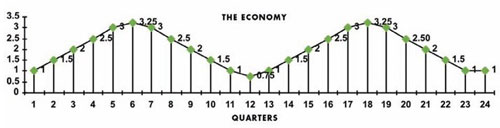

So what's the big deal? Why does Company C represent a riskier situation? It has a lot to do with the economy. The graph ("The Economy") depicts two points on my "figurative" representation of the economy.

The situation characterized in the graph represents an expansionary economy: the focus is on growth, both in sales and in profits. The problem occurs when this growth (whether profitable or unprofitable) occurs primarily with borrowed funds as a source of money to buy the assets to create the sales. When this process gets out of control, debt usually increases faster than net worth and the financial risk occurs in two areas: 1) increasing interest charges, which can erode operating profit and cash; and 2) further strains on cash flow required to service an increasing principal burden.

The pattern works fine as long as the economy (or a particular industry) experiences an "up" pattern, as shown in Q1-Q6 and Q12-Q18 on the graph. The pattern changes, however, when the economic picture trends downward, as shown in Q6-Q12 and Q18-Q24.

In a downturn, sales and profits are squeezed as the market declines and highly leveraged firms feel the pinch soonest. In a desperate attempt to salvage cash flow, they cut price to increase market share, but sacrifice profit.

For most of these firms, this action has the effect of making the situation worse, but there are really very few alternatives. Although it's tough on everyone, it's toughest on all of the Company C's. For them, the downward trends on the graph represent a new chapter in their businesses: Chapter 11. When the "downside" of the economic cycle occurs, the focus shifts from a "sales and profit" orientation to one of survival. That's the value of a strong balance sheet (strong as in not too much debt). Those firms with less debt and more net worth have what I call "staying power": a better ability to withstand adversity. (This is a euphemism for a continuing ability to generate cash when you're down.)

If you move each of my three composite firms to the two downturns shown on the graph and project a negative ROA of minus 10 percent, what happens? Since each firm has 100 of assets, each firm will then lose 10 (-10% of 100 = -10). So Company A experiences a net worth decrease of 90 to 80; Company B experiences a net worth decrease from 50 to 40; and Company C experiences a net worth decrease from 10 to 0.

The successful businesses I work with have an innate "gut feeling" about how to manage this process. They know that debt equals risk and that risk is a function of greed. From the cyclical nature of the economy, they know that you make money on the upswings--so they don't get too greedy (or leveraged). Without the high levels of debt, they are then able to survive the inevitable downturns and become more than a "one cycle" firm.

The real key, as I mentioned before, is that this internal pattern is controllable. Manage the balance sheet as well as the income statement, because volume alone is not the answer--especially when it comes at the expense of increasing debt and increasing leverage. Remember, financially speaking, a lever works both ways.

Steve LeFever is the chair of Business Resource Services (BRS). For over 10 years franchisors and franchisees have improved their financial performance by following the BRS Profit Mastery process: financial training, performance benchmarking, and accountability/bankability modeling. Contact him at 800-488-3520 x14 or [email protected].

Share this Feature

Recommended Reading:

FRANCHISE TOPICS

- Multi-Unit Franchising

- Get Started in Franchising

- Franchise Growth

- Franchise Operations

- Open New Units

- Franchise Leadership

- Franchise Marketing

- Technology

- Franchise Law

- Franchise Awards

- Franchise Rankings

- Franchise Trends

- Franchise Development

- Featured Franchise Stories

FEATURED IN

Multi-Unit Franchisee Magazine: Issue 1, 2011

$550,000

$200,000

Franchising.com is produced by Franchise Update Media. Franchise Update Media has its finger on the pulse of franchising with unrivalled audience intelligence and market driven data. No media company understands the franchise landscape deeper than Franchise Update Media.

P.O. Box 20547

San Jose, CA 95160

PH. (408) 402-5681

The multi-unit franchise opportunities listed above are not related to or endorsed by Multi-Unit Franchisee or Franchise Update Media Group. We are not engaged in, supporting, or endorsing any specific franchise, business opportunity, company or individual. No statement in this site is to be construed as a recommendation. We encourage prospective franchise buyers to perform extensive due diligence when considering a franchise opportunity.

The multi-unit franchise opportunities listed above are not related to or endorsed by Multi-Unit Franchisee or Franchise Update Media Group. We are not engaged in, supporting, or endorsing any specific franchise, business opportunity, company or individual. No statement in this site is to be construed as a recommendation. We encourage prospective franchise buyers to perform extensive due diligence when considering a franchise opportunity.

Copyright © 2001 - 2025. All Rights Reserved. Legal Notices | Privacy Policy