The Myth of Multiples: Beware of Over-Reliance on EBITDA

Whether the mergers and acquisitions market is in a hot upswing or in a down cycle, one valuation measure remains the primary focus in nearly all transactions: the multiple of EBITDA (or cash flow).

This seems to be universally true, as it is used by buyers, sellers, finance sources, franchisors, franchisees, investment banks, and private equity groups. In more than 23 years of managing M&A activity in the franchise sector, we continue to scratch our heads at the overemphasis and focus on EBITDA multiples. This article explores what we describe as "The Myth of Multiples," and how deal-makers put too much emphasis on this inconsistent measure of value.

While the arithmetic to calculate a multiple is simple (transaction price divided by EBITDA), the variables in the calculation are not quite so simple. The transaction price is rarely as straightforward as a single number, and the trailing 12-month EBITDA has more inputs than we can possibly evaluate in this article. More important, the multiple based on the trailing 12-month EBITDA is much less important than a measure capturing the performance improvement a new owner may achieve going forward.

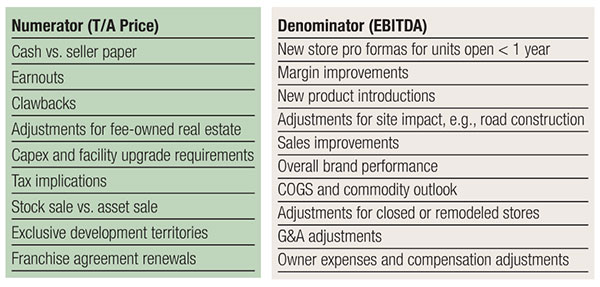

Calculating a multiple is a somewhat arbitrary measure involving numerous variables, adjustments, assumptions, and inputs. The measure involves both quantitative and qualitative factors, which 1) are different in every transaction, and 2) tend not to be uniform across brands, franchise systems, or segments of the industry. More specifically, common factors that may affect the numerator (transaction price) and denominator (EBITDA) are shown in the table. As you can see, the multiple calculation is not quite as easy as it may first appear.

Other key factors

At least as important to the transaction process and valuation is quantifying how the buyer can improve the business and its cash flow, the walkaway proceeds a seller will earn, and the potential for continuing liabilities the seller may face. Here are four examples we've observed in recent transactions:

- A franchisee purchases units from a long-time operator in a system that had a reputation for high sales and low margin results. The seller had near-zero debt and was content with the cash flow from the business, reducing the motivation for the seller to tightly manage operations. The buyer paid a high single-digit multiple for the business. Upon closing, the buyer initiated technology upgrades and new manager incentives to help drive the bottom line. In this transaction, the buyer increased the value of the business by more than 50 percent in one year. The effective multiple was much lower after one year.

- A buyer purchased stores from a franchisor for what appeared to be a very high multiple. However, with knowledge of the seller's labor grid, pricing, and the market, the buyer was able to initiate new systems that resulted in almost 10 points of margin improvement in Year 1. In addition, because of the buyer's effective management of labor and traffic flow, stores were staffed properly at peak hours, resulting in significant sales improvements. The effective multiple turned out to be less than 50 percent of the original transaction multiple in a short time.

- An independent casual dining concept sells its brand for a 10x multiple, and the seller is quite proud of this. Unfortunately for the seller, the astute buyer was able to negotiate a significant adjustment in the tax basis for the assets, a clawback for failing to achieve aggressive and unrealistic growth projections, and have the seller keep a significant interest in the company for a second bite of the apple (and to keep skin in the game). With declining performance after the sale and a couple of weak new store openings, the adjusted sales price one year after the sale translated to a multiple closer to 6x. In addition, the seller was faced with an unhappy financial partner, wholesale turnover of staff dictated by the buyer, and a rather unpleasant working environment under the new regime. While the primary still had substantial proceeds from the sale, it won't soon be recognized as an authority on creating maximum deal value.

- A franchisee buys a group of restaurants in an adjacent market from a longtime franchisee in the same system. The buyer felt there were G&A synergies, margin opportunities, sales upside associated with image improvements, pricing opportunities, and other enhancements based on the fact that the buyer was considered to be a "better operator." The buyer was confident that he had paid a fairly low multiple for the business. Unfortunately, the buyer soon discovered that the seller did a much better-than-anticipated job of squeezing margins out of operations. What's more, the adjacent market did not allow for pricing increases, several higher-volume stores had new competition, and the new image enhancements fell flat. All this occurred while the brand was experiencing a cyclical decline. What appeared to be an attractive multiple ballooned to a high single-digit multiple post-closing, putting not only the acquisition but the parent company at risk for a default. The buyer clearly had not done his homework and set himself up for a difficult situation. In this situation, the seller had agreed to a lower multiple from this buyer based on lower escrow requirements, no seller paper, and an all-cash deal. After one year, the post-close multiple didn't look so good.

In conclusion, it is vitally important to understand that using an EBITDA multiple to value a transaction can be a dangerous thing unless all the variables and nuances are properly factored into the equation. This is a classic example of, "It just isn't that simple." The EBITDA multiple can be a valid indicator of value, but only when used correctly. Don't let a myth become a miss.

Dean Zuccarello, CEO and founder of The Cypress Group, has more than 30 years of financial and transactional experience in mergers, acquisitions, divestitures, strategic planning, and financing in the restaurant industry. The Cypress Group is a privately owned investment bank and advisory services firm focused exclusively on the multi-unit and franchise business for more than 23 years. Contact him at 303-680-4141 or [email protected].

Share this Feature

Recommended Reading:

FRANCHISE TOPICS

- Multi-Unit Franchising

- Get Started in Franchising

- Franchise Growth

- Franchise Operations

- Open New Units

- Franchise Leadership

- Franchise Marketing

- Technology

- Franchise Law

- Franchise Awards

- Franchise Rankings

- Franchise Trends

- Franchise Development

- Featured Franchise Stories

FEATURED IN

Multi-Unit Franchisee Magazine: Issue 1, 2014

$350,000

$30,000

Franchising.com is produced by Franchise Update Media. Franchise Update Media has its finger on the pulse of franchising with unrivalled audience intelligence and market driven data. No media company understands the franchise landscape deeper than Franchise Update Media.

1201 New York Avenue NW, Suite 300A

Washington, DC 20005

PH. (408) 402-5681

The multi-unit franchise opportunities listed above are not related to or endorsed by Multi-Unit Franchisee or Franchise Update Media Group. We are not engaged in, supporting, or endorsing any specific franchise, business opportunity, company or individual. No statement in this site is to be construed as a recommendation. We encourage prospective franchise buyers to perform extensive due diligence when considering a franchise opportunity.

The multi-unit franchise opportunities listed above are not related to or endorsed by Multi-Unit Franchisee or Franchise Update Media Group. We are not engaged in, supporting, or endorsing any specific franchise, business opportunity, company or individual. No statement in this site is to be construed as a recommendation. We encourage prospective franchise buyers to perform extensive due diligence when considering a franchise opportunity.

Copyright © 2001 - 2025. All Rights Reserved. Legal Notices | Privacy Policy